Over the past two weeks, I am reading some truly astonishing news about the state of American finance in 2024, and how American Credit Card debt has reached record-breaking levels!

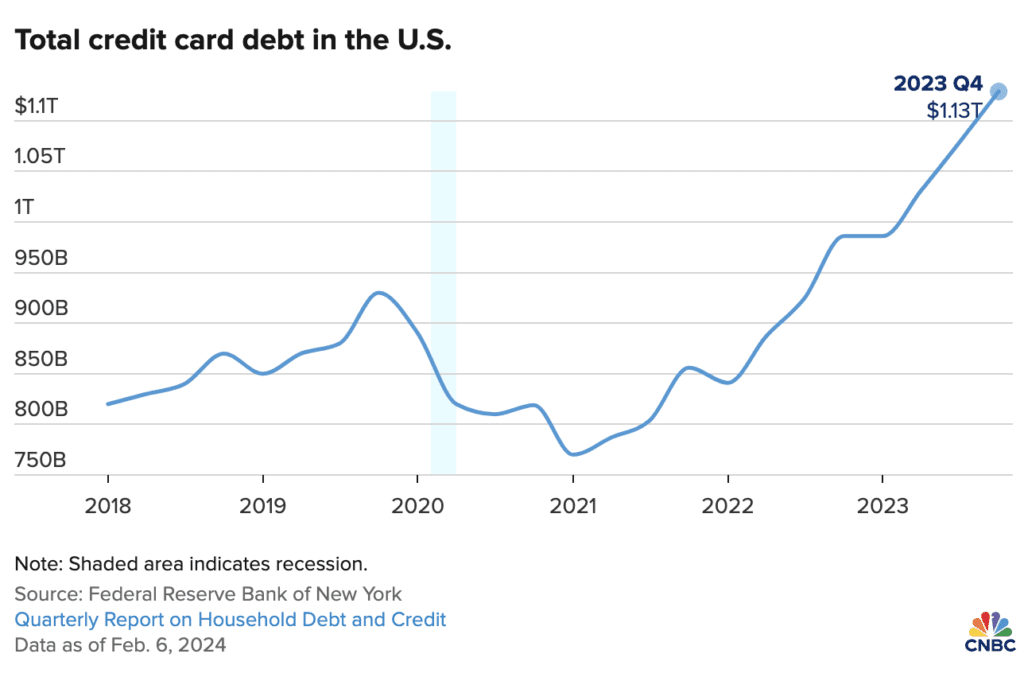

The CNBC article notably reported in the United States, average credit card balances have jumped 10% from 2022, to a record $6,360 average credit card debt in 2023, an all-time high according to a report from TransUnion (the credit rating company).

Some of the statistics in the article were astounding:

- On the topic of Average Prime Rate in Interest: “The average credit card charges a record high 20.74%, according to Bankrate.”

- Interest Rates in 2024 are debilitating for many: “At more than 20%, if you made minimum payments toward the average credit card balance, it would take you more than 17 years to pay off the debt and cost you more than $9,000 in interest, Rossman calculated.”

- Americans now owe a combined $1.13 trillion on their credit cards, according to the Federal Reserve Bank of New York

- On the topic of Credit Card deliquencies, these “surged more than 50% in 2023, the New York Fed reported,” and ” ‘serious delinquencies,” or those 90 days or more past due, reached the highest level since 2009″ according to TransUnion.

As if this wasn’t enough confirmation, last week I read another article which confirmed the extent of the American debt crisis.

This article provided even more astounding data:

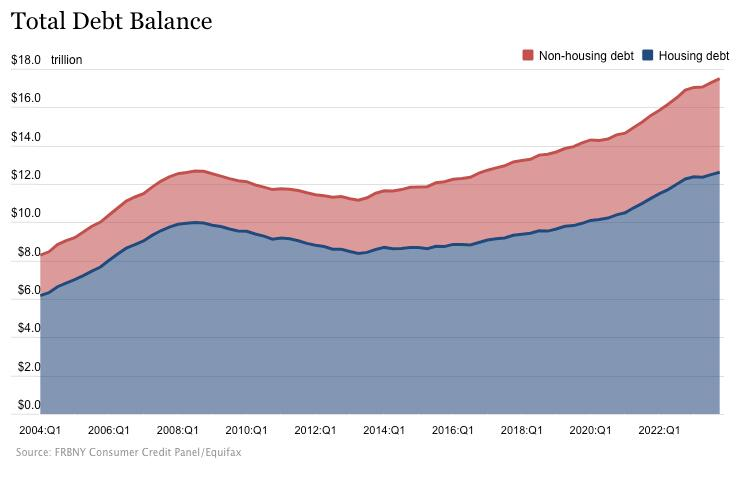

- Americans haven’t just been borrowing using credit cards. Every debt category increased in the fourth quarter of 2023.

- Mortgage balances increased by $112 billion and stood at $12.25 trillion at the end of the year.

- Auto loan debt rose by $12 billion to $1.61 trillion in Q4 and stands at $1.61 trillion.

- Other consumer debt balances, including department store credit cards and other consumer loans, grew by $25 billion.

- Student loan balances were comparatively flat in Q4, rising by $2 billion.

- Aggregate delinquency rates rose by 3.5 percent, with approximately 8.5 percent of credit card balances and 7.7 percent of auto loans transitioning into delinquency.

- Serious delinquencies (more than 90 days past due) are the highest since 2011.

- According to the Consumer Financial Protection Bureau, nearly one-tenth of credit card users find themselves in “persistent debt.” This means they rack up more interest and fees each year than they pay toward the principal

At Oscape, we support and affirm living a free life full of possibility – in business, in travel, and in lifestyle. To achieve such a lifestyle, it also means avoiding credit card debt!

My Experience With Credit Card Debt

Credit cards are one of the most expensive and least efficient ways to borrow money. This is especially true in 2024, and will be so for the foreseeable future.

While I am currently and intentionally credit card debt free for several years, this was not always the case.

In 2011 I entered a period where I thought it was okay to hold credit card debt, and only pay the minimum payments while building up a moderate balance. By 2012 this outlook had ballooned into nearly $4000 USD in running credit card debt.

By 2016, I still hadn’t learned a lesson, and spending without consequence I reached approximately $12,000 USD in debt. Then in mid-2016 my primary income source was comprimised, and I continued to spend without proper income to back it up or pay off balances.

By the end of 2017, I was at nearly $36,000 USD in credit card debt, the maximum I reached. At this point, my debt had reached a real crisis point – and on top of this, I ran out of wiggle room to transfer debt to zero interest credit cards.

In the end, it took over two years to pay this debt off, during which time I continued to pay exorbitant interest rates on this massive balance. I was only saved because my income was again high, and I channeled every spare dollar and cent I could to paying it off as fast as possible.

Then again in 2019 to 2020, I entered another period of extreme debt. This was partially a result of the pandemic, but admittedly it was also an effect of my lifestyle choices at the time.

In this round, my debt topped out at ~$12,000 USD. At this point I had learned a valuable lesson from my earlier experience, and I tackled my debt problem head-on, and quickly. I paid this off by pulling some money out of investments to pay off half the debt balance, and then transferred the other half to a zero percent interest card for 15 months. I calculated and then maintained consistent monthly payments until it was fully paid prior to interest beginning.

Not wanting to experience the prior years misery, I paid off all my balances in 2021. I’ve been debt free since, and refuse to hold any credit card debt no matter the circumstance.

Avoid Credit Card Debt Like A Plague

Having experience five figure credit card debt twice in my life, and also having successfully paid off both instances twice, I can tell you the best way to have no credit card debt is to avoid it entirely! At this stage the pain of credit card debt is simply not worth the satisfaction of whatever that debt will buy me.

Credit Card Debt Reduces Your Happiness

It’s now well studied that financial stress reduces anyone’s levels of happiness, and this is especially true when it comes to credit card debt.

According to data from Happy Money, “overspenders report 44.3% higher levels of financial stress than savvy spenders, who spend less than they bring in each month….“

“Positive cash flow is associated with countless financial and psychological benefits,” said Dr. Chris Courtney, cognitive neuroscientist and Senior Vice President of Science, Risk, and Analytics at Happy Money. “It’s important to spend less than you bring in each month and find your right balance between saving and spending.”

This article also includes excellent data on happiness and stress levels that follows with no debt:

- Happy Money data shows those with no credit card debt experience nearly 50% less financial stress than those with $5,000 or more in credit card debt

- People who regularly contribute to savings accounts report 10% less financial stress than those who do not.

- Individuals with at least $400 in savings report 16.9% higher levels of life satisfaction than those without that amount saved.

Credit Card Debt Reduces Your Freedom

Paying down and avoiding your debts can fundamentally change your life and give you a sense of freedom – you’re entirely free to spend your money how and when you want to.

In a choice quote in another CNBC article by Tara Falcone of Reason, “Individuals that are completely debt free absolutely have a different mindset. There’s a greater sense of peace, freedom and opportunity that comes with being debt free…Not owing anyone anything or being beholden to anyone offers debt-free individuals more options and control over every dollar they own. When you have no debt, you’re able to, with 100% freedom, decide how and when to spend your money.”

It goes without saying that having no debt, especially in credit cards, gives you a profound sense of financial freedom. Such individuals are also far more careful about jumping back into debt!

I Pay Off All My Credit Cards Early

From my own exposure starting one decade ago, and then again five years later, I learned the hard and best ways of managing debt. By far the best way against debt circumstances to avoid it entirely!

These days, I pay off my credit card balances twice a month. I do this before the statements are even delivered, so that my statement balance due usually comes in at under $50 each month.

Another reason I pay off my credit card balances early, is to have wiggle room in case my income falters for one billing cycle. Because credit cards release statements once a month, and these are due a month later, you have approximately 60 days grace to pay a balance with no interest. Paying this early gives you that additional leeway of 30-60 days in case it’s ever needed!

I also use Mint to link all my accounts across the board, and closely track my spending and budget at least once a week. I like the Mint app to be able to see all my account balances at once in one place, so I know that I’m not spending more than I actually have coming in.

Tackle Your Credit Card Debt Systemically

What if you’re not credit card debt free already?

Certainly this is the more difficult path, but it’s not impossible either. Proper reduction of credit card debt requires a combination of tough choices, smarter choices, and consistent discipline with both managing your finances, as well as paying off your debt.

The only way to tackle your existing credit card debt is to address it systemically. That means above all, you need to be disciplined and pay off the balance consistently each month until it’s all gone.

One of my favorite tools that I learned from my own experience is to simply take your balance, divide it by the number of months you wish to pay off your debt in, and then use that number as your annual monthly pay off budget. Do this payment consistently each month, and you’ll pay off that card systemically.

Consolidate Credit Card Debt Into Zero Interest Cards

One of my favorite methods to pay off credit card debt consistently without incurring additional interest is to open a new, zero-interest credit card, and balance transfer my entire debt balance into that card (or more cards if needed). Although this usually incurs a 3% balance transfer fee, that’s far better than paying a 20% APR each month.

I take the balance $$ value I transferred, and divide it by the timeline of the zero-interest period. This determines the monthly pay-off budget without incurring additional interest. For example, if you hold a $1000 debt balance, zero interest for 10 months, you’ll need to make $100 monthly payments consistently over those ten months to avoid additional interest and debt!

Once completed, affirm your own minimum monthly payment, to make sure these balances are paid off before interest hits hard. Sometimes even if you aren’t able to finish the full pay-out, you can repeat this process with another, different Zero Interest card.

Use Your Points to Reduce Credit Card Debt

I am surprised when I hear some people hold credit card debt, but also carry six figure points balances and don’t use them for what they can be used for! Credit card points can be used not just for travel, but also for daily expenses and for special deals you can take advantage of.

If you’re holding a massive stash of points as well as significant credit card debt, you should absolutely be using your points to reduce your credit card debt!

Some excellent free cards such as the Chase Freedom Flex, Chase Freedom Unlimited, or the Bank of America Business Advantage Travel Rewards card, offer excellent cash-back prospects for any consumer and business owner. These cash back rewards will reduce your balance due on new statements, allowing you to redirect those funds to paying off your debt.

Reduce Your Credit Cards If You Have Too Much Debt

Rather than sticking to multiple expensive premium cards with high annual fees, consider dropping down to the No-Annual-Fee version of each credit card. Every issuer offers various levels of credit card, and there’s nearly always a free option available. It’s better to use the same funds to pay your existing debt, than to pay a high annual fee for more points on spending.

Alternatively, another possibility is to reduce your credit card count to a single, high performance card you can charge all your transactions to. American Express Platinum and Chase Sapphire Reserve are popular options.

Ask Your Credit Card Issuer for a Lower Annual Percentage Rate

If you don’t have the option of being approved for Zero Interest Cards, the next best option is to ask your card issuers for lower APRs on the remaining debt. All you need to do is call your credit card issuer and make this request, stating your difficulties in managing the existing balance.

From the same first CNBC article, it is reported “76% of people who asked for a lower interest rate on their credit card in the past year got one, according to a LendingTree report.

Increase Your Income

The last and final tip to reduce your credit card debt is also exceptionally important, and rarely talked about. That final tip is to increase your income, by all means necessary. This may mean asking your boss for a raise, finding a new higher paying job, or even holding multiple jobs for a while.

Increasing your income will help you pay your debt off faster – you’ll simply have more revenue that you can channel towards paying off your debt. Combined with reducing your lifestyle expenses and transferring to zero interest cards, this is a debt-killer trifecta combo!

Paying your debt faster will also build upon itself like a snowball, and eventually you’ll have both no debt AND all that additional income coming in, to use as you please!

Change Your Lifestyle

The key procedure for reducing debt to manageable level is also to reduce your lifestyle and economic costs. Often Americans end up in persistent credit card debt because their lifestyle choices far exceed their actual capacity to pay the incurred debt. This is especially true in 2023 and 2024, an era of sky-high inflation.

One of the first things I target for cost reductions is consistent subscriptions and fees that burden debt, but don’t provide value in raising income and revenue. TV subscriptions such as HBO Max or YouTube Premium tend to make good targets, reducing average monthly expenses. I avoid delivery services and even eating out or joining social events, in such circumstances.

In times of rough finances, I’ve even cut subscriptions such as Amazon Prime, electing instead to simply walk or drive to a store to get what I need to buy.

Final Thoughts on Credit Card Debt

Remember above all that your debt is a short term thing, but only if you let it be and manage it correctly.

Paying off your credit card debt consistently will improve your happiness and freedom, just as it will massively raise your credit score.

Having credit card debt can be a miserable experience. The stress, and the lack of confidence in your personal financial condition can make anyone stressed out and miserable on a very human level.

The best way to reduce your credit card debt is to tackle it systemically and consistently, with a clear pay-off target goal strategy in place.